Navigating Foreclosure in Greenville County: A Step-by-Step Guide for Homeowners

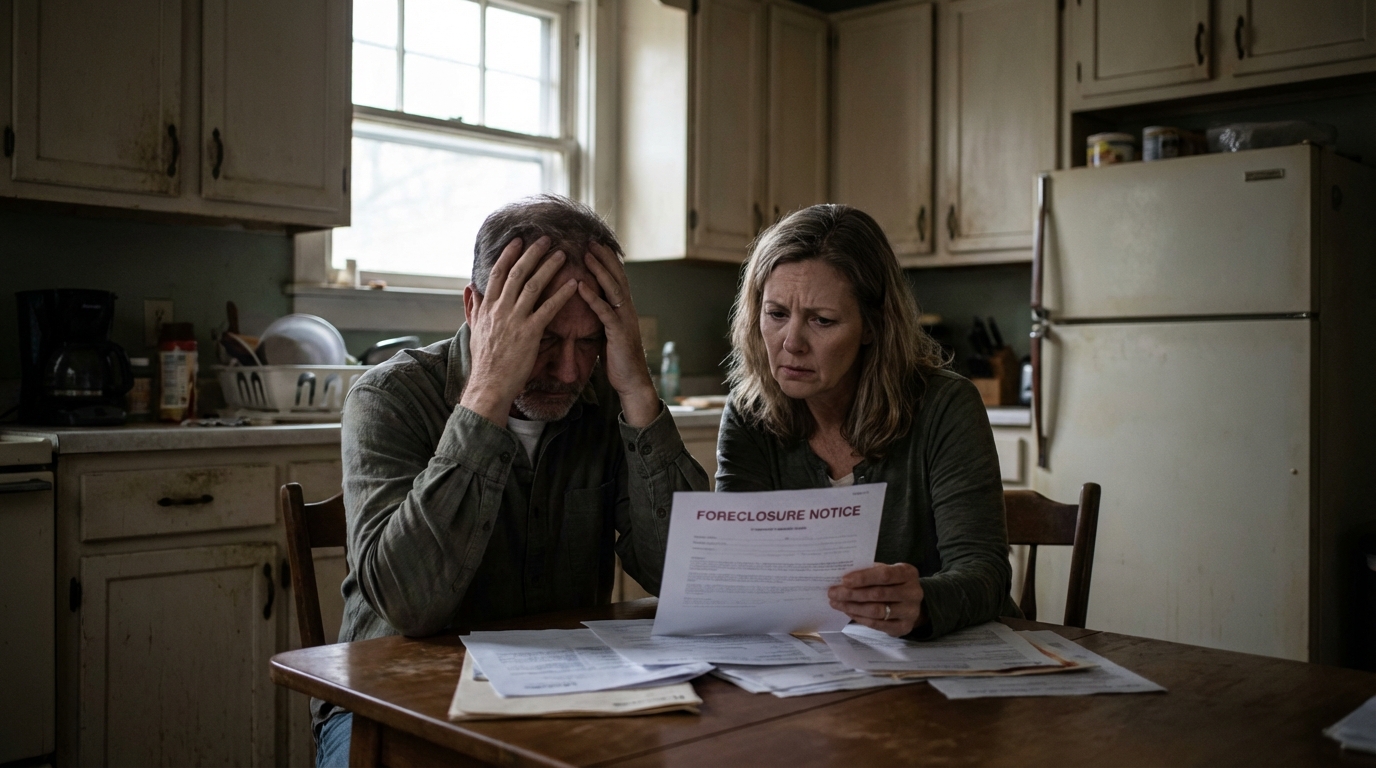

Receiving a notice of foreclosure can feel like the world is crashing down around you. The stress, uncertainty, and fear are overwhelming. If you're a homeowner in Greenville County facing this challenge, please know you are not alone, and you have options. This isn't just about a property; it's about your home, your family, and your future. Our goal is to walk you through the process with clarity and empathy, empowering you to make the best decision for your unique situation.

Whether you're in a historic home near Augusta Road or a family house in Simpsonville, the path forward starts with understanding the road ahead. Let's break down the South Carolina foreclosure process step-by-step.

Understanding the South Carolina Foreclosure Process

South Carolina is a “judicial foreclosure” state. This means the lender must file a lawsuit and get a court order to foreclose on your property. This process takes time, which gives you a window to act. Here’s what the timeline typically looks like in Greenville County:

1. The Pre-Foreclosure Period & Notice of Default

Foreclosure doesn't begin the day you miss a payment. Federal law generally requires the lender to wait until you are more than 120 days delinquent before starting official proceedings. During this time, they will send letters and make calls. This is your first and best window to communicate with your lender about loss mitigation options.

2. The Lawsuit is Filed (Lis Pendens and Summons)

If no resolution is reached, the lender's attorney will file a lawsuit with the Greenville County Clerk of Court. You'll be served with a Summons and Complaint. This is a formal legal document, and it's crucial not to ignore it. You typically have 30 days to file an “Answer” with the court. It’s highly recommended to consult with a housing counselor or an attorney at this stage.

3. The Master-in-Equity Hearing

Your case will be referred to a special judge called a Master-in-Equity. A hearing will be scheduled where the lender presents its case. If you don't respond or defend yourself, the judge will likely issue a default judgment, granting the lender the right to sell your home.

4. The Foreclosure Sale

The Master-in-Equity will sign a Foreclosure Order, and a public auction for your home will be scheduled. These sales are often held at the Greenville County Courthouse. The property is sold to the highest bidder, which is frequently the lender itself.

Important Note: Even after the sale, it's not immediately over. South Carolina has an “upset bid” period, which allows another party to place a higher bid within a specific timeframe after the initial auction, potentially extending the process.

Your Options for Avoiding Foreclosure in Greenville

Seeing the process laid out can be intimidating, but knowledge is power. The most important thing you can do is take action. Ignoring the problem will not make it go away. Here are several proactive paths you can explore:

- Loan Modification: You can negotiate with your lender to permanently change the terms of your loan to make payments more affordable. This might involve lowering the interest rate or extending the loan term.

- Forbearance or Repayment Plan: If your financial hardship is temporary (e.g., a short-term job loss), you might qualify for a forbearance, which temporarily suspends or reduces your payments. A repayment plan allows you to catch up on missed payments over a set period.

- Short Sale: If you owe more on your mortgage than your house is worth, your lender might agree to a short sale. This allows you to sell the home for less than the outstanding balance, and the lender forgives the remaining debt. This is complex and requires bank approval.

- Deed in Lieu of Foreclosure: You voluntarily transfer the property's title to the lender in exchange for being released from your mortgage obligation. This also requires lender approval and isn't always an option.

A Proactive Solution: Selling Your House for Cash

For many homeowners in Greenville, the traditional real estate market isn't a viable solution during foreclosure. The timeline is too long, the need for repairs is too costly, and the uncertainty of a buyer's financing falling through is too risky. This is where selling your house for cash to a reputable local home buyer can be a powerful alternative.

Why a Cash Sale Can Help

- Speed and Certainty: A cash sale can close in as little as 7-10 days. This speed is critical to paying off the mortgage before the bank forecloses, protecting your credit from the severe damage of a foreclosure record.

- Sell 'As-Is': Is your roof leaking or your HVAC on its last legs? These are major roadblocks in a traditional sale. We buy houses in any condition. You don't need to spend a dime on repairs or even clean up. From Travelers Rest to Mauldin, we handle it all.

- No Commissions or Closing Costs: You avoid the 6% realtor commission and we typically cover all closing costs. The cash offer you receive is the amount you walk away with.

- Regain Control: A cash sale puts you back in the driver's seat. You choose the closing date and move forward on your own terms, not the bank's. It allows you to walk away with dignity and, in many cases, cash in your pocket to start fresh.

Take the Next Step for Your Future

Navigating foreclosure in Greenville County is one of the toughest challenges a homeowner can face. But you have the power to change the outcome. By understanding the process and exploring all your options, you can find the path that leads to the best possible future for you and your family.

If you're feeling the pressure and want to learn more about a simple, fast, and transparent way to resolve your situation, Central Valley REI is here to help. We provide fair, no-obligation cash offers for homes across Greenville. Contact us today for a confidential chat to see how we can support you. There's no pressure, just a clear solution designed to give you peace of mind.